Meet Fuel MCP: talk to Claude about any financial decision

.png)

From what we see working with our clients, most businesses, whether they're making $3M or $50M, are still guessing when it comes to real financial planning.

If you're anything like them, you take last year's revenue, bump it by 25%, and call it a plan. Three months later, you're wondering why the numbers don't add up and cash flow feels tight despite hitting your targets.

This pattern repeats like the Lion King's Circle of Life. After working with 500+ SMBs from $2M to $50M, I have found that the same seven planning challenges keep appearing. So let me show you how to fix them.

You set an annual revenue target of $10M. Great. But how do you get there? Most teams can't answer that question beyond "sell more" and "hire people."

A real plan connects your revenue target to the specific actions that generate it (think SMART goals). If you need $10M in business income and your average deal is $50K, you need 200 deals. If your close rate is 25%, you need 800 qualified leads. If your lead-to-opportunity conversion is 40%, you need 2,000 marketing leads.

Now you have a comprehensive financial plan. Marketing knows they need to generate 2,000 leads. Sales knows they need to close 200 deals. Those numbers drive hiring decisions, budget allocation and daily priorities.

Running out of cash usually comes from ambitious business plans without the operational step-by-step to support them—costly mistakes that proper business financial planning could have prevented.

You spend two weeks building an annual plan in December. By March, reality has diverged completely from your forecast, after yet another economic downturn and a bunch of unexpected expenses, but nobody updates the numbers. By June, the plan is irrelevant.

The best-run SMBs treat planning as a continuous process, not an annual event. They review actual performance against the plan monthly, identify gaps and adjust the financial goals and forecast based on what happened. This catches problems early when you can still do something about them and helps you avoid costly mistakes that derail business growth.

Weekly reviews take it further. You track key leading indicators (pipeline velocity, burn rate, churn signals) every week, so you spot trends before they become crises. This doesn't mean rebuilding your entire comprehensive business budget weekly. It means checking if you're on track and flagging anything that needs attention.

Sales forecasts $3M in new business. Marketing plans to generate enough leads for $2M. Product is building features for a $5M target. Nobody notices the disconnect until it's reporting season and everyone's blaming everyone else for missed targets.

Cross-functional planning means all departments work from the same assumptions and targets. Sales pipeline feeds into the revenue forecast. Marketing spend ties to expected lead volume. Hiring plans connect to growth projections and cash flow capacity.

This requires a single source of truth for your business finances. It doesn't mean everyone uses the same spreadsheet (though that helps). It means financial planning connects to operational execution, so department leaders can see how their decisions affect company-wide performance and long term financial success.

Your Q1 forecast said $750K. You actually did $500K. Now what? Most teams either ignore the gap or panic, but neither response helps.

The right move is reforecasting. You close the books on Q1, analyze why you missed (was it pipeline volume, conversion rate, deal size, timing?), and adjust your Q2-Q4 forecast based on current reality rather than wishful thinking.

This sounds obvious, but many entrepreneurs resist it. Reforecasting feels like admitting failure. In reality, it's the only way to make informed decisions about the rest of the year. Should you cut business expenses? Adjust hiring plans? Double down on what's working? You can't answer these questions without an updated forecast that reflects your actual financial situation.

See also: Revenue Forecasting Software Comparison

You review cash flow statements monthly and notice revenue dropped 15%. That's helpful, but it's a lagging indicator. By the time it shows up in your financials, the problem has been building for weeks.

Leading indicators predict future performance before it hits your financial statements. Pipeline coverage dropping below 3x quota signals revenue problems three months out. Customer engagement scores declining predict churn before it happens. Time-to-hire increasing suggests you'll miss your hiring targets.

Set up a weekly review process that tracks these leading indicators. When something crosses a threshold (pipeline drops below $X, gross margin falls under Y%), you trigger a specific response before the problem compounds and threatens your financial foundation.

Your annual plan lives in a spreadsheet. Your projects live in Asana or Monday. Your financials live in QuickBooks. Your CRM is Salesforce. None of these systems talk to each other, so your financial plan has no connection to actual business operations.

This creates two problems. First, updating your forecast requires manually copying data from multiple sources, which takes hours and introduces errors. Second, your team can't see how their daily work connects to financial objectives, so they make decisions in a vacuum.

The solution is integration. Your financial planning software should pull data automatically from your CRM and integrate with your accounting system, project management tools, and payroll platform. This eliminates manual data entry and creates real-time visibility into how projects, sales and operations affect your financial success.

Time-consuming processes create two problems. First, you delay important decisions because the analysis takes too long. Second, you avoid updating your plan regularly because it's too much work, which means you're constantly working from outdated information.

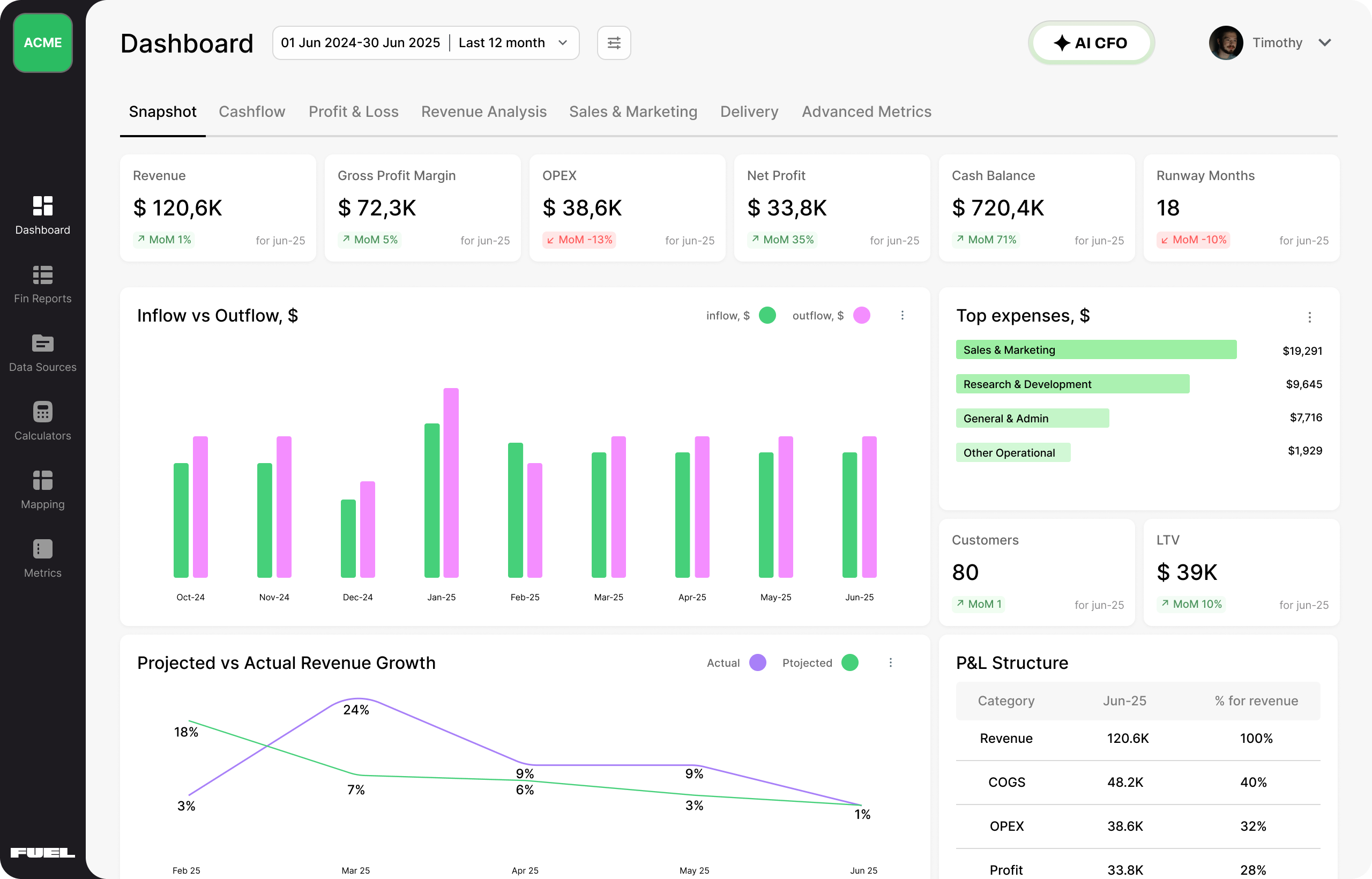

Modern financial planning for entrepreneurs should enable faster, not slower decision-making. Fuelfinance's AI-powered forecasting creates baseline and optimistic projections in minutes rather than hours. our natural language dashboard creation means you describe what you want to see and the system builds it, no training required. Automated scenario modeling tools let you test "what if" questions instantly.

The goal isn't eliminating human judgment. It's eliminating the manual grunt work so you can focus on analysis and decision-making instead of data wrangling — essential for maintaining business continuity during your entrepreneurial journey.

The pattern is consistent. Companies that break through to $10M, $20M, $50M and beyond all do it differently when it comes to financial planning and cash flow management:

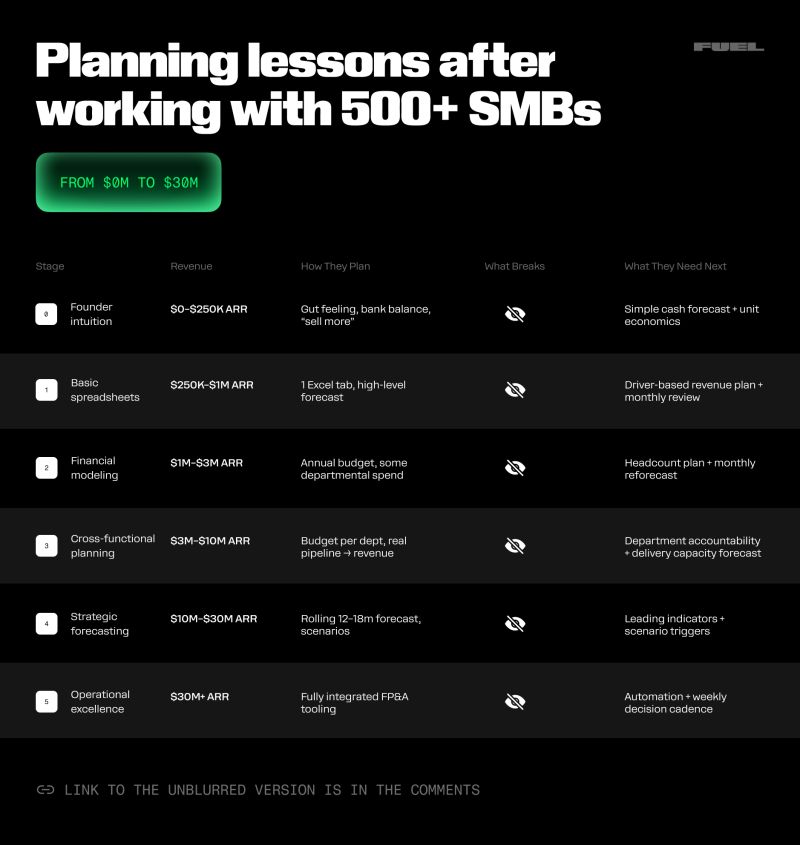

I know it's easier said than done. What you need at $500K ARR is completely different from what you need at $10M. So here's a customized financial plan for businesses at different stages.

Download it here or keep reading for a more detailed walkthrough.

You're running on gut feeling and bank balance checks. "Sell more" is the entire strategy.

What breaks: Cash shocks, unmanaged churn, random spending.

What you need: Simple cash forecast and basic unit economics. Track money in, money out, and whether you make profit on each customer. This is also when you should establish separate accounts for personal and business finances to avoid mixing personal funds with business operations.

You have one Excel tab with a high-level forecast. You can see three to six months ahead.

What breaks: Assumptions aren't tied to reality. Your forecast says $100K next month because it feels right, not because the pipeline supports it.

What you need: Driver-based revenue plan and monthly reviews. Connect forecasts to actual metrics like lead volume and conversion rates. Start thinking about your business structure and whether your current entity type supports your growth plans.

You've got an annual budget with departmental spend tracking. You're thinking in quarters now. Good job!

What breaks: Runway surprises and hiring inefficiency. You approve roles without modeling the cash impact.

What you need: Headcount planning and monthly reforecasting. Model every hire's full cost before posting the job offer. This is when many entrepreneurs start working with business partners, a financial advisor or certified financial planner to ensure they're balancing personal financial well being with business growth demands. An outsourced CFO would be a good choice.

The company has set budgets per department and a pipeline connected to revenue projections. Teams are mostly aligned.

What breaks: Forecast disconnects and margin uncertainty. You're hitting revenue targets but don't know which customers or services actually make money.

What you need: Department accountability and delivery capacity forecasting. Track profitability by customer, product and channel. Start implementing proper risk management strategies and ensure you have adequate insurance coverage for your growing operations.

Rolling 12-18 month forecasts with scenario planning are the standard. You can model "what if" scenarios before committing to one of them.

What breaks: Slow reaction to market changes. You only update quarterly, so you're months behind on trends.

What you need: Leading indicators and scenario triggers. Define metrics that predict problems and build automatic responses. This stage often requires working with wealth management professionals and solid financial modeling software with anomaly detection alerts.

Fully integrated FP&A software is an integrated part of your company. All departments work from the same forecast. You catch anomalies in real-time.

What breaks: Fragmented systems. Great processes, but data lives in twelve places and requires manual compilation.

What you need: Automation and weekly decision cadence. Integrate systems so data flows automatically.

Need more inspiration? Check out Lovable's insane ARR growth story.

Most founders waste months evaluating software they don't need yet or that won't actually fix their problems.

Spreadsheets break down once you hit $1M-$2M and have multiple team members.

Generic FP&A and accounting tools designed for enterprises bring complexity you don't need.

Point solutions that handle one piece (like sales forecasting or expense management) create new integration headaches.

You end up with eight tools that don't talk to each other, making the fragmentation problem worse and complicating your ability to maintain accurate cash flow statements.

You need purpose-built software like Fuelfinance that solves the seven planning challenges without enterprise overhead. Here's what you get:

That, plus Fuelfinance implementation takes about two weeks, according to our clients. Let's chat.

You don't need to solve all seven planning challenges today. Start with understanding where you are and what needs your attention first.

Our planning stages cheat sheet shows you exactly what matters at your stage, what typically breaks, and where to focus.

Most importantly, it helps you avoid the trap of implementing solutions for problems you don't have yet or ignoring the ones that are about to break your business.

The best financial plan isn't the most sophisticated one. It's the one you'll actually use to make better decisions, allocate resources effectively, and grow without stress.

Stop guessing. Start with clarity about where you are and what you need next. Trust me, the path from here to financial independence and business success will becomes much clearer.

Book a demo to see how we can support you every step of the way.

Open separate accounts (separate bank accounts and credit cards) for business on day one. Pay yourself a regular salary from the business account to your personal account. That's it.

The complication comes from mixing personal financial goals and business matters and trying to untangle them later. Document any transfer between accounts with a clear note about what it was for.

This separation protects both your personal and business assets, simplifies tax filing (reducing the complexity of your taxable income), and gives you accurate visibility into real business performance versus your personal goals.

Profit is revenue minus expenses on paper. Cash flow is actual money moving in and out of your accounts.

You can be profitable and still run out of cash if customers pay slowly, you have large upfront expenses, or you're growing fast and need to invest ahead of revenue. Many profitable businesses fail because they couldn't make payroll despite strong income statements — financial challenges that proper cash flow management could have prevented.

For entrepreneurs, cash flow matters more in the short term because it determines whether you can keep operating. Profit matters more long-term because you need sustainable economics. Track both, but watch cash flow weekly and profit monthly to maintain financial freedom and avoid the costly mistakes that sink otherwise healthy businesses.

The 50/30/20 rule is a personal financial planning framework, not a business one. It suggests spending 50% of after-tax income on needs, 30% on wants, and 20% on savings, retirement accounts, investment objectives and debt management.

For business owners balancing personal assets and business finances, the principle of allocating resources systematically still applies. Many successful entrepreneurs aim to keep operating expenses at 70-80% of revenue, leaving 20-30% for growth investment and building an emergency fund — a financial safety net that protects against unexpected situations.

The specific percentages matter less than having a conscious allocation strategy that balances current operations, growth investment, and building financial stability for both your business and personal financial situation.

Before $1M ARR: Use software with expert support or a fractional advisor for 5-10 hours monthly ($2K-$5K/month). You don't have enough complexity to justify more.

$1M-$3M ARR: Add a financial controller or FP&A manager internally. You need someone who can build forecasts, model scenarios, and work cross-functionally.

$3M-$10M ARR: A fractional CFO (part-time, experienced) will provide strategic guidance without full-time cost and can help with tax planning, risk management strategies, and ensuring adequate insurance coverage.

$10M+ ARR: Full-time CFO makes sense. You're dealing with investor relations, sophisticated capital decisions, potential M&A, and need senior financial expertise driving strategy. They often coordinate with wealth management professionals for estate planning and help establish retirement plans for personal and business needs.

You can always keep it simple and switch to Fuelfinance that gives you proprietary AI-boosted FP&A software with financial professionals' help for a fraction of the price.

Just imagine how that would transform your team’s productivity and focus? Talk to our financial experts to know more.