Meet Fuel MCP: talk to Claude about any financial decision

Are you struggling to figure out the right moment to record revenue and keep up with accounting standards?

You're not alone – many new business owners face the same challenge.

Understanding revenue recognition and when and how to record revenue will significantly impact your financial reporting and overall business finances management.

For startups, it also helps boost investor trust and stay compliant with international financial reporting standards and regulations.

Keep reading to discover revenue recognition principles, examples and tips for different business models.

Before talking about the revenue recognition concept, it's essential to distinguish between revenue and cash, as these terms sound similar at first glance.

Cash is what customers pay you – the money that lands in your bank account.

On the other hand, revenue is earned when you deliver the product or service that was paid for, which doesn't necessarily coincide as the payment can be made before or after providing the service.

Even if you receive the cash upfront, you only count it as revenue once you've provided the service that the customer paid for.

Until then, this money is recorded as deferred revenue in your accounts. This ensures that you recognize revenue only when you've fulfilled your obligation to the customer, regardless of when you receive the payment.

This distinction is critical to accurate reporting and understanding your business's financial health. Now, we can move on to explaining revenue recognition.

The revenue recognition principle, a fundamental, generally accepted accounting principle (GAAP), outlines how and when revenue should be recorded in financial statements.

According to this principle, revenue ought to be recognized when goods are delivered or services performed, indicating that the transaction is complete and the income can be accurately reported.

The revenue recognition principle, also known as accrual accounting, ensures that financial statements reflect the actual value of goods and services provided by a company during a specific period.

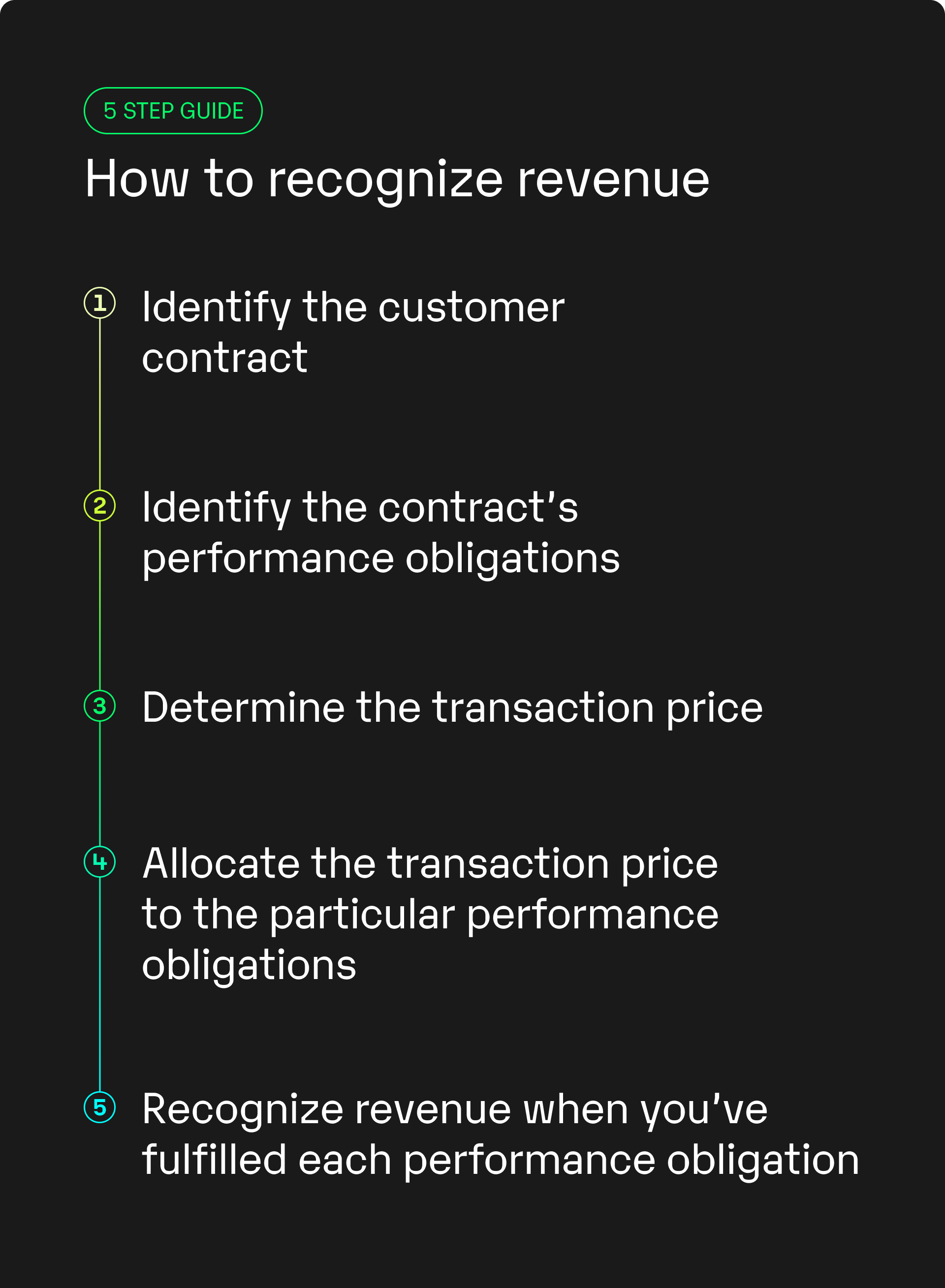

There are different revenue recognition methods, but we'll now show you how to do it according to the 5-step revenue recognition standard approved by IFRS:

1. Identify the customer contract: Before you start, you must first identify your agreement with the customer, whether a formal signed document or a simple verbal agreement. Every contract should meet specific requirements – it must be a business deal between two parties outlining the payment terms, what each party gets and what they must do. Essentially, both sides should clearly understand what they agreed to. This clarity is essential in accounting to accurately show when revenue should be recorded.

2. Identify the contract’s performance obligations: Before recognizing revenue in accounting, understand your responsibilities to the customer. A performance obligation refers to specific goods or services you promised to deliver. These goods or services are distinct if they can be identified separately on a receipt or invoice.

Let’s use a bakery as an example. Handing over one pastry for a specified price is a distinct performance obligation. However, it's not always that straightforward, especially in services. A product or service must be usable or beneficial independently, separate from other items in the agreement. For instance, if you sell a vacuum cleaner and offer an additional warranty only available with the vacuum, the warranty isn't considered a separate performance obligation.

3. Determine the transaction price: When you exchange money with a customer for a product or service, the total amount is the transaction price. It can also include other factors like discounts or the right to return items. This concept applies not just to physical goods but also to services or software companies. Customers need to understand their options if they're unsatisfied with a service. Clear terms about refunds and cancellations are vital for transparency and customer satisfaction.

4. Allocate the transaction price to the particular performance obligations: You should determine the cost of each performance obligation or each item. This process is called allocating the transaction price. When each product or service has a clear and separate price, allocating the total transaction amount is easy. However, some factors like discounts or incentives can change the final price. In that case, you estimate how much these affect the overall revenue. This estimation is based on what's most likely to happen, which is called the expected value.

5. Recognize revenue when you’ve fulfilled each performance obligation: You should only recognize revenue after you've fulfilled your part of the deal with the customer and provided the desired products or services (remember deferred revenue?).

The good news is that some parts of the process can be automated using the right financial planning software tools, as we'll explain in a separate section below.

But before we get into that, let’s use real-life examples to illustrate what it actually means to recognize revenue and when and how to do it.

Now, let's take a look at some revenue recognition examples to help you understand when to recognize revenue based on your business model:

Imagine having an IT company that distributed its software as a one-time software package installed on the customer's local hardware instead of running a SaaS product with recurring payments.

If a customer buys and receives the software in the same month, the company can record the sale and recognize the entire revenue in that month, even if it costs over $10,000. This simplifies the revenue recognition process.

The most popular SaaS financial model is subscription-based. Customers pay for software either monthly, quarterly or annually. Their chosen plan gives them access to the company's services for the next period.

Let's consider an example of a customer who paid one year upfront. Even though the company received the money for the entire year, it can't immediately count all of it as revenue.

Instead, they need to spread out the revenue recognition processes over the entire year as they deliver the service each month. This SaaS method is called recognizing revenue on a straight-line basis.

Two key revenue metrics help SaaS companies recognize their revenue – MRR and ARR.

Monthly Recurring Revenue (MRR) represents the total amount of regular income from monthly subscriptions or services. This metric is standard in subscription-based businesses and SaaS companies.

On the other hand, Annual Recurring Revenue (ARR) is a measurement that can help you track the total anticipated income from ongoing subscriptions over annual reporting periods. The formula for calculating ARR is multiplying your MRR by 12.

P.S. To learn more about the KPIs you should track, check out our comprehensive guide on SaaS agency metrics.

If you're selling physical products like hardware, payment and delivery don't usually happen simultaneously. Customers pay upfront, but you can recognize that payment as revenue only after the products reach them, which usually takes some time.

To illustrate it with an example: a company sells an appliance to a customer in April, the customer pays in May, but the appliance reaches the customer in June. The company should recognize revenue in June, although the customer had paid for the appliance some months before the delivery.

Service-based businesses and consultants should recognize the revenue once they provide the service.

For example, if you provided services to a client in January, but the client only paid for them in April, it doesn't matter. You still have to record and recognize them in January even though you have not received the payment yet.

Alternatively, you can recognize revenue gradually or proportionally based on the services provided over time (especially for long-term services).

In the context of a marketplace GMV (gross merchandise volume) represents the total value of transactions. However, the only revenue that can be recognized is the portion of GMV that the marketplace operator earns as fees, which is usually just a fraction of GMV.

Imagine you run an online marketplace and the total GMV on your platform is $100,000. This number includes all sales made by sellers, regardless of whether the transactions are completed or if any fees are deducted.

However, your revenue as the marketplace operator comes from the fees you charge sellers for using your platform.

Let's say your platform charges a 10% fee on each transaction. This means your revenue is 10% of GMV, so the money you get to keep and recognize as revenue equals $10,000.

Here are just some of the reasons why it's essential to follow good revenue recognition practices:

If you're struggling to keep up with revenue recognition standards, we've got you covered.

Fuelfinance offers a unique combination of financial management software designed for startups at any stage and unlimited support from our team of financial experts, who act as your outsourced CFO.

We can help you with the entire revenue recognition process and meet revenue recognition criteria. Fuelfinance gives you recommendations on the best revenue recognition method for your business, plus in-depth revenue analytics. Let’s say you have regular recurring revenue from subscriptions and one-off revenue to add to that. We’d analyze both and suggest the right way to track them.

However, we don’t stop there. Our tool can do much more, covering everything you need for small business financial management. That includes cost analytics, unit economics, cash flow analytics, KPI tracking and P&L metrics.

Here are some of Fuelfinance key features:

And if you're on a limited budget, keep reading because there's more.

We've developed Bootstrap, a free financial management solution for startup founders in the early stages before securing funding. It can help you simplify finances and generate professional reports for investors.

Here's what you can do for free:

At Fuelfinance, we understand the challenges of starting a business. That's why we've developed a user-friendly financial management tool specifically designed for small businesses and startup founders. The tool makes it easy to handle your finances without expertise.

With Fuelfinance, you can quickly generate your financial plan and receive ongoing support from our team of experts, including help with revenue recognition.

Book a demo today to see how Fuelfinance can automate your finances.

Here are the IFRS reporting standards criteria for revenue recognition:

According to generally accepted accounting principles, revenue is recognized when it's earned, meaning when the goods or services get delivered to the customer, and not necessarily when the cash is received.

IFRA reporting standards criteria suggest the 5-step revenue recognition model explained in the article above. IFRS also suggests clearly defining contracts and performance obligations in a written form, accurately estimating transaction prices and being transparent with stakeholders.

Yes, according to IFRS 15, revenue can be recognized before invoicing if the performance obligations are satisfied, or in other words if you've already provided goods or services.

Just imagine how that would transform your team’s productivity and focus? Talk to our financial experts to know more.